[Disclaimer: the analysis and views expressed in this article are solely my own unless stated otherwise.]

In the fall of 2016, I became an angel investor by officially joining Maple Leaf Angels(MLA). It is quite the experience to have moved to the “other side of the table” after 5 years of hustling and bootstrapping. My motivations are to support the startup community, keep a close eye on tech trends, and of course make financial returns. Since then, I have built up a pipeline that allowed me to attend over 150 pitches, coach dozens of startups, and place a handful of investments. Also, many more startup pitches have passed through my inbox via the official MLA process or through other sources like VCs, directly from entrepreneurs, or referrals.

I do get asked about my experiences and the type of startups that I see, so I decided to share my analysis and views here. The total number of startups in this analysis is 265. For added perspective, I spoke with some entrepreneurs to try to better understand the lay of the land.

Overall, I feel the number of startups in the pipeline is indicative of the status Toronto is claiming as tech and entrepreneur hubs. I met an amazing group of entrepreneurs who come from a variety of backgrounds, people with dreams to change the status quo and make a difference in this world. On the other hand, the analysis below raises some serious concerns about the state of Toronto’s startup ecosystem.

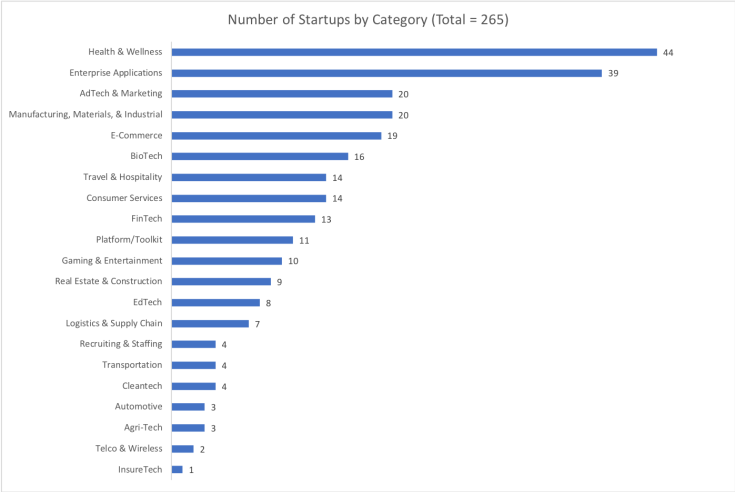

Here is a chart breaking down the 265 startups by category:

Healthcare rules

According to the numbers, Toronto is a mecca for health and wellness startups. The city is home to healthcare-centric incubators such as Johnson & Johnson’s JLABS, St. Michael’s Biomedical Zone, and U of T’s Health Innovation Hub. Add to that the many research hospitals and their staff, it’s no surprise that health and wellness startups sat at the top of the chart.

So what types of startups did I see? Tele-medicine, diagnostics, patient care, and hospital/clinic management software were well represented. There were also a couple of digital wellness companies that I think represent the beginnings of a strong trend in rationalizing how people interact with their devices to limit our growing dependency on them.

Entrepreneur’s Perspective:

I spoke with a healthcare entrepreneur about my findings and this is what they had to say:

- The Entrepreneur was surprised by the high number of healthcare startups. Logically, with their attractive case for profitability, Enterprise Applications/SaaS startups should be the dominant category.

- Early stage grant funding could explain a large number of healthcare startups (especially in Toronto), however, subsequent angel or VC funding is not easy compared to Boston (America’s health capital). Toronto’s angels and VCs seem to be put off by healthcare’s complicated path to profitability and are, therefore, less comfortable with this sector than their Boston counterparts.

- Toronto being a health research hub with a large number of researchers and medical doctors along with the abundance of grants could have fuelled the number of health-related startups. A deal flow analysis, looking at subsequent rounds of investments and assessing business continuity, might reveal a very different picture.

It’s not easy for FinTechs

Toronto is ranked as one of the top financial centers in the world, yet, surprisingly, only 5% of the startups in my analysis were FinTechs. In comparison, the figure is 12% out of those startups housed at the DMZ (I consider the DMZ to be a microcosm of Toronto’s startup ecosystem). Still, I would consider 12% to be low for Toronto, especially given the strong buzz coming from the banks on innovation investments and initiatives.

There must be barriers and challenges that resulted in the not-too-many number of FinTechs. Here’s how one FinTech entrepreneur put it:

Entrepreneur Perspective:

- The Entrepreneur immediately began telling me how it is hard to work with the big Canadian banks. It’s a big barrier with many FinTechs having a low likelihood of landing a partnership with any of those banks. Conversely, the entrepreneur was able to cold call a US financial institution and land a partnership.

- Complicating the situation, Canadian banks are siloed from within and it’s an arduous task to find out who to talk with and who makes partnership decisions.

- Regulations in Canada add friction. Canada is still studying the merits of open banking policies which are an important catalyst for advancements in financial services. However, we are lagging behind the UK and Europe who have already enacted such standards a few years ago. In the US, big banks are actively establishing data sharing deals. “We are 5 years behind the States and 10 behind London”, said the Entrepreneur.

- Moreover, with their highly publicized innovation and digital investments, banks are actively poaching tech talent directly from startups. The Entrepreneur provided me with an example, I have also seen this happen on other occasions. While a free talent market should exist, the gold standard should be for banks to actively partner with startups instead of competing with them over precious resources.

Where are the insurance startups?

I chose to categorize InsurTechs separately from FinTechs. Globally, the technology innovation momentum within insurance is rapidly growing. Startups are promising to disrupt the insurance model across the supply chain, from product development to underwriting to claims management. The consultancies have published a lot of thought-leadership on the topic, and it seems that every respectable insurance carrier must have an innovation team housed in a colourful office with bean bag chairs.

Only 1 out of the 265 startups in my analysis is a pure-play InsurTech. So what is going on? Let’s hear from an insurance entrepreneur:

Entrepreneur Perspective:

- Most of the insurance innovation in Canada has been limited to the distribution side of the business. Which is easy to replicate and tough to scale. Adopting a nervous approach, most insurance carriers have focused on upgrading the broker experience with some forays into direct selling to consumers.

- The heavy regulations in Canada are pushing back innovative insurance entrants. For example, peer-to-peer insurance startups are thriving in the US and Europe but have yet to make an appearance in Canada. The Entrepreneur also explained to me how hard it was to obtain licenses necessary to sell policies.

- London and New York provide their startups with a more mature ecosystem with investors making big bets on insurance. By contrast, very few Toronto VCs are excited about insurance and generally speaking there is limited risk-taking in the space. The biggest InsurTechs will not come out of Toronto. China, with its massive market and pioneering micro-insurance startups, will lead.

- The Entrepreneur asked an important rhetorical question: “Could two people with no insurance backgrounds set up a company like Lemondae in Canada?”. The answer is most likely a “No”. Canadian entrepreneurs face an ecosystem that is risk-averse and that overemphasizes the importance of industry experience.

- Finally, the Entrepreneur expressed their frustration with all the talk about “thinking outside the box”. The reality is very different. This became evident to me when a manager who works for one of Canada’s largest insurance companies told me that their innovation group has yet to deliver anything of value and were undergoing an “identity crisis”.

Big companies should do more

The fact that Canadians are more risk-averse and lagging behind others in tech adoption has been discussed ad nauseam. It, unfortunately, is a reality from the perspective of the entrepreneur.

The problem is complex and involves policymakers, industry leaders, and the investor community. I think the best place to start would be at the big companies. Banks and insurers should make it easy for startups to partner with them, they can also influence regulators and policymakers. Startups are much more agile and creative than the big companies, they can come up with new products and services at a much faster pace. But startups need big companies to access data, customers, and funding. A robust startup intake model should be adopted. Cross-functional company representatives can meet and assess startups on a regular basis. I’ll cover this in more detail in a future post.

There are many hard-working entrepreneurs in Canada taking risks and sacrificing a lot to solve important problems. What they need is support from the rest of us.